How can an SMSF borrow money to purchase real property?

An SMSF is permitted to borrow funds to acquire an asset provided that the borrowing is structured as a limited recourse borrowing arrangement (LRBA).

This article explains the superannuation and taxation laws applicable to limited recourse borrowing arrangements entered into on or after 7 July 2010. Different rules may apply to arrangements entered into prior to that date.

The information provided in this enclosure is general in nature and does not address your particular circumstances. You should seek specific advice on your particular situation.

How does an LRBA work?

Apart from very limited exceptions, an SMSF is only permitted to borrow under an LRBA. Broadly, for a borrowing to constitute an LRBA all of the following conditions must be met:

- The borrowed monies must be applied towards the acquisition of a single acquirable asset

- The asset must be an asset which the SMSF is permitted to acquire under the prevailing law

- The acquired asset must be held on trust for the benefit of the SMSF

- The SMSF must have a right to acquire the legal ownership of the asset by making one or more payments

- The rights of the lender or any other party involved in the arrangement (for example, a guarantor) are limited to the rights relating to the acquired asset (that is, the loan is limited recourse)

It is important that an SMSF’s borrowing meet all of the above conditions. Failure to do so may cause the SMSF to cease to be a complying superannuation fund and when this occurs significant adverse tax consequences are triggered. These consequences include loss of the tax concessions available to complying superannuation funds (for example, the 15% tax rate) and a 45% tax on the market value of the assets of the fund that do not represent non-concessional contributions.

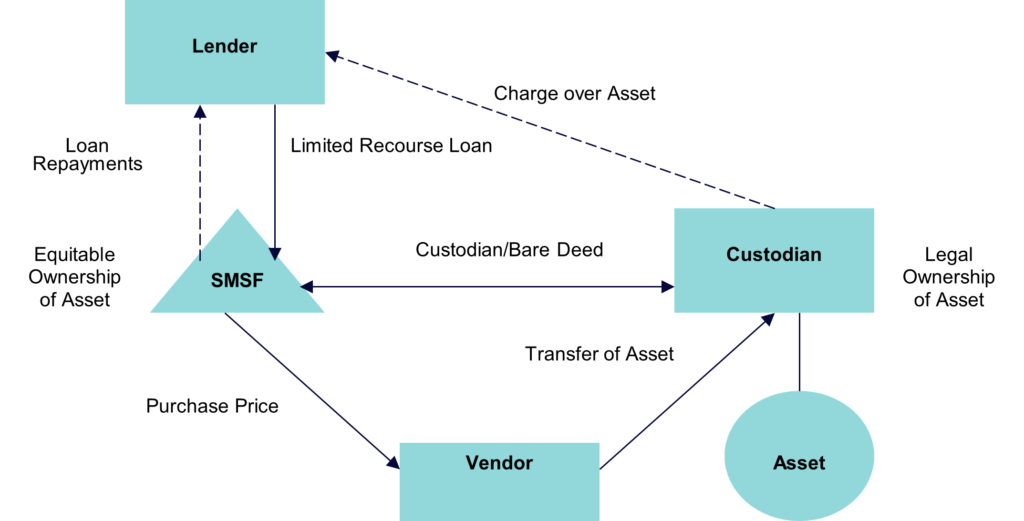

A limited recourse borrowing arrangement can be diagrammatically represented as follows.

Under an LRBA, an SMSF borrows funds from a lender on a limited recourse basis so as to acquire an asset (generally real estate) under an arrangement whereby the legal title to the asset is held on trust by a custodian for the benefit of the self managed superannuation fund during the term of the loan.

Typically the lender will take a charge over the legal title to the asset during the term of the loan to secure its loan. This generally takes the form of a registered mortgage where the asset constitutes real property.

The “single acquirable asset” rule

The single acquirable asset rule relates to the acquisition of a single asset or a collection of assets that are considered a single acquirable asset. This rule is crucial when an SMSF is involved in borrowing arrangements, such as an LRBA, to acquire real property.

The Australian Taxation Office (ATO) ruling SMSFR 2012/1 (SMSFR 2012/1) provides guidance on the application of the “single acquirable asset” rule. SMSFR 2012/1 clarifies the following key items:

- Definition of a Single Acquirable Asset: a single acquirable asset can be a single object of property or a collection of objects that are inseparable (physically or legally).

- Examples and Scenarios: The ruling provides examples to illustrate different scenarios where an asset is considered a single acquirable asset. For instance, a single title of land with a house is typically a single acquirable asset, whereas multiple titles without a unifying physical object of significant value (for example, a house) spanning across all titles would not be considered a single acquirable asset.

What else can the borrowing be used for?

Besides using the borrowed monies to acquire the asset, an SMSF is also permitted to use funds borrowed under an LRBA to pay expenses incurred in connection with the acquisition and borrowing. This includes conveyancing fees, transfer duty, brokerage and loan establishment fees.

Borrowed funds may also be used to maintain and repair the asset the subject of the LRBA. A distinction needs to be made between repairing the asset and improving the asset. An SMSF may not use borrowed funds to improve the asset. The distinction between an improvement and a repair can sometimes be difficult to determine.

SMSFR 2012/1 also provides specific guidance on this issue:

- Maintenance/Repairs vs. Improvement: Maintenance and repairs are actions taken to prevent deterioration or to fix defects in the asset, ensuring it remains in its original condition. These activities do not enhance the asset’s value or alter its fundamental character. Improvements on the other hand refer to changes or additions to an asset that enhance its value, extend its useful life, or alter its fundamental character.

- Examples:

- Repairs: Fixing a leaking roof, replacing broken windows, or repairing damaged fixtures are considered repairs. These activities restore the asset to its original condition without changing its character

- Maintenance: Regular activities such as painting, cleaning, or servicing equipment to prevent deterioration are classified as maintenance

- Improvements: Adding a new room or upgrading fixtures to a higher standard than the original would be considered improvements and are not permissible under an LRBA

SMSF trustees must ensure that any borrowed funds used for maintenance or repairs do not inadvertently result in improvements. Proper documentation and clear distinction between maintenance/repair and improvement activities are essential for compliance.

Do you need help?

If you would like any assistance with understanding how an SMSF can borrow funds to acquire real property (i.e., real estate in the form of a single acquirable asset), please get in touch with our team of SMSF experts. Our lawyers have advised most of Australia’s leading SMSF lenders and so, are well-placed to advise you!

Table of Contents

Posted in SMSF